Overview:

IRS offers every

taxpayer the option to itemize their deductions or to claim the standard

deduction. Standard deduction amount varies depending on your filing status.

However, if you have significant deductible expenses during the year, the total

of which is greater than your standard deduction, you can itemize by reporting

the expenses on Schedule A. Itemized Deductions will help you to reduce federal

tax liability if it is more than Standard Deduction.

Generally speaking, individuals on higher tax brackets have more to gain

from itemizing their deductions. For example, many people list interest on a

mortgage payment as a large deductible in the “interest you paid” section.

Obviously, a wealthier home owner will have paid more interest on their home

than a poorer one.

Purpose Of

Schedule A

Like the standard tax returns, itemized deductions are

subtracted from the adjusted

gross income (AGI) to arrive at an

individual's taxable income. Schedule A is required in any year you choose to

itemize your deductions.

The schedule has seven categories of expenses:

1. Medical and dental

expenses.

2. Taxes.

3. Interest.

4. Gifts to charity.

5. Casualty and theft

losses.

6. Job expenses and

certain miscellaneous.

7. Other Miscellaneous

Deductions.

Each of these categories has different requirements and

limitations on the amount you can deduct.

Taxpayer can claim those deductions which he/she is eligible

to claim and no need to complete each section as one single section may be

enough to be more than standard deduction. You can notice the table of Standard

Deductions according to your filing status on left side top corner of Form

1040, page 2.

Example

1

– For tax year 2015, $6,300 is the eligible amount of Standard deduction for

those who file their filing status as ‘Single’. If you have spent $2,000 for

charity and $2,000 for mortgage interest, your total itemized deductions will

be $4,000 which is less than $6,300 of standard deduction amount. So, opting

for higher deduction (i.e., standard deduction of $6,300 is beneficial)

Note: The mortgage

interest deduction alone can be quite significant and by itself be greater than

the standard deduction.

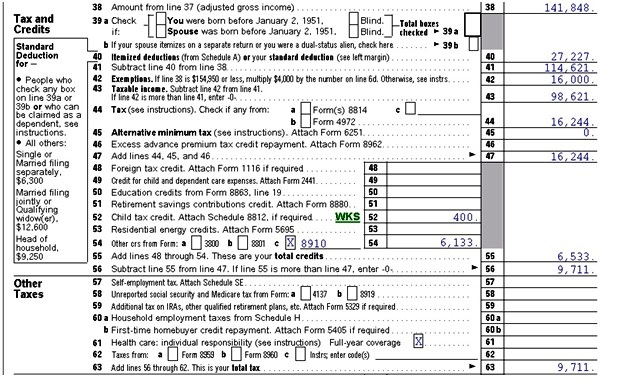

After all calculations, if itemized deductions are more than

standard deductions, the total deduction should be transferred to line 40 of Form

1040.

Part I:

Medical and Dental Expenses (Pub 502)

This deduction will be claimed usually if unreimbursed

medical and dental expenses are more. Both of the below conditions should be

met in order to deduct your medical and dental expenses:

a. If you itemize

deductions on Schedule A.

b. If your expenses are

more than 10% of your AGI or 7.5% of your AGI for taxpayers 65 years or older.

If a question arises as what all a taxpayer can deduct?

Answer is as below:

Any medical condition which includes the cost of following:

·

Mitigation.

·

Cure.

·

Diagnosis.

·

Treatment.

·

Prevention.

·

Items needed for above purposes, including

ü

Equipment

ü

Supplies.

ü

Diagnostic Devices.

These are some of the expenses that you can deduct under medical and dental section:

Ø Cost of medical care

from any of these practitioners

o

Acupuncturists

o

Chiropractors

o

Dentists

o

Eye doctors

o

Medical doctors

o

Occupational therapists

o

Osteopathic doctors

o

Physical therapists

o

Podiatrists

o

Psychiatrists

o

Psychoanalysts giving medical care

o

Psychologists

o

Other qualified medical

practitioners

Ø

Transportation costs to and from

medical care. If you drive your own car, the deduction is 23 cents per

mile in 2015. (Medical miles deduction)

Ø

Prescription medicines

Ø

Amounts you paid for qualified

long-term care services

Ø

Limited amounts you paid for any

qualified long-term care insurance contracts

Ø

Medical insurance premium -- You

can't deduct pre-tax salary contributions you make to an employer-sponsored

health insurance plan.

Ø

Amounts you pay if not covered

by Social Security for:

o

Medicare B supplemental insurance

o

Medicare D insurance

o

Medicare A premiums

You usually can't deduct premiums

you pay for certain types of policies. This is true of policies with benefits

that aren't tied to the actual cost of the medical care you received. These

policies:

Ø

Pay you a certain amount (Ex: policy

that pays you $200 a day while hospitalized)

Ø

Pay you for lost earnings

Ø

Pay a flat amount for the loss of a

limb or eyesight

The required contributions you make

to state disability-benefit funds might not be medical expenses limited by the

10% rule -- 7.5% if 65 or older. This is true if you contribute to:

Ø

Alaska Unemployment Compensation

Fund

Ø

California Paid Family Leave Program

Ø

California Non occupational

Disability Benefit Fund

Ø

New Jersey Non occupational

Disability Benefit Fund

Ø

New Jersey Unemployment Compensation

Fund

Ø

New York Non occupational Disability

Benefit Fund

Ø

Pennsylvania Unemployment

Compensation Fund

Ø

Rhode Island Temporary Disability

Benefit Fund

Ø

Washington State Supplemental

Workmen’s Compensation Fund

Instead, include these payments as a part of your state tax

deductions on Schedule A.

These are some of the expenses that you cannot deduct under medical and dental section:

Ø

Cosmetic surgery not related to any

of these:

o

Congenital abnormality

o

Accident

o

Disease

Ø

Medicare tax on wages and tips paid

as part of the self-employment tax or household employment taxes

Ø

Nursing care for a healthy baby

Ø

Usually, drugs not approved by the

FDA

Ø

Funeral, burial, or cremation costs.

Source Document: Generally amounts

spent on medical and dental will be provided by taxpayer himself.

Input:

Print Preview in lacerte tax software: